Loan Compound Interest Calculator

Calculating compound interest on loans can be a complex and time-consuming process, but it's essential to understand the true cost of borrowing. A Loan Compound Interest Calculator is a valuable tool that helps individuals and businesses determine the total interest paid over the life of a loan. By inputting key details such as principal amount, interest rate, and loan term, users can quickly and accurately calculate the total cost of their loan, making informed decisions about their financial situation. This calculator simplifies the process, saving time and reducing financial stress. Accurate calculations are crucial for smart financial planning.

- Understanding the Loan Compound Interest Calculator

- How do you calculate compound interest on a loan?

- What is 6% interest on a ,000 loan?

- What is the compound interest on 00 at 6.75% compounded daily for 20 days?

-

Frequently Asked Questions (FAQs)

- What is the Loan Compound Interest Calculator and how does it work?

- How do I use the Loan Compound Interest Calculator to calculate my loan payments?

- What are the benefits of using the Loan Compound Interest Calculator?

- How can I use the Loan Compound Interest Calculator to plan my finances and make informed decisions about my loan?

Understanding the Loan Compound Interest Calculator

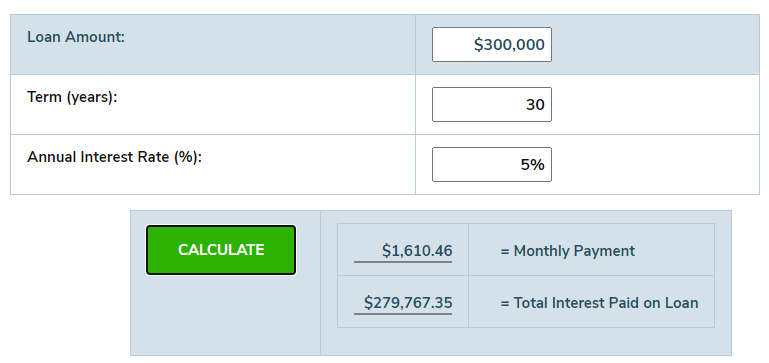

The Loan Compound Interest Calculator is a financial tool used to calculate the total interest paid over the life of a loan, taking into account the principal amount, interest rate, and compounding frequency. This calculator is essential for borrowers to understand the true cost of their loan and make informed decisions about their financial obligations. The Loan Compound Interest Calculator can be used for various types of loans, including mortgages, car loans, and personal loans.

How the Loan Compound Interest Calculator Works

The Loan Compound Interest Calculator works by using a formula that takes into account the principal amount, interest rate, loan term, and compounding frequency. The formula calculates the total interest paid over the life of the loan, as well as the monthly payment and total amount paid. The calculator can also be used to compare different loan options and determine which one is the most cost-effective.

Benefits of Using a Loan Compound Interest Calculator

Using a Loan Compound Interest Calculator can help borrowers in several ways. Firstly, it helps to save money by identifying the most cost-effective loan option. Secondly, it reduces financial stress by providing a clear understanding of the loan's terms and conditions. Thirdly, it increases financial transparency by providing a detailed breakdown of the loan's costs and payments.

Key Components of the Loan Compound Interest Calculator

The Loan Compound Interest Calculator consists of several key components, including:

| Component | Description |

|---|---|

| Principal Amount | The initial amount borrowed |

| Interest Rate | The rate at which interest is charged |

| Loan Term | The length of time the loan is outstanding |

| Compounding Frequency | The frequency at which interest is compounded |

| Monthly Payment | The amount paid each month |

Example of How to Use the Loan Compound Interest Calculator

For example, let's say you want to borrow $10,000 for 5 years at an interest rate of 6%. Using the Loan Compound Interest Calculator, you can calculate the total interest paid over the life of the loan, as well as the monthly payment and total amount paid. The calculator will provide you with a detailed breakdown of the loan's costs and payments, helping you to make an informed decision about your financial obligations.

Comparison of Different Loan Options Using the Loan Compound Interest Calculator

The Loan Compound Interest Calculator can also be used to compare different loan options and determine which one is the most cost-effective. For example, you can compare the costs of a fixed-rate loan versus a variable-rate loan, or compare the costs of a loan with a longer loan term versus a shorter loan term. By using the calculator to compare different loan options, you can make an informed decision about which loan is best for your financial situation.

How do you calculate compound interest on a loan?

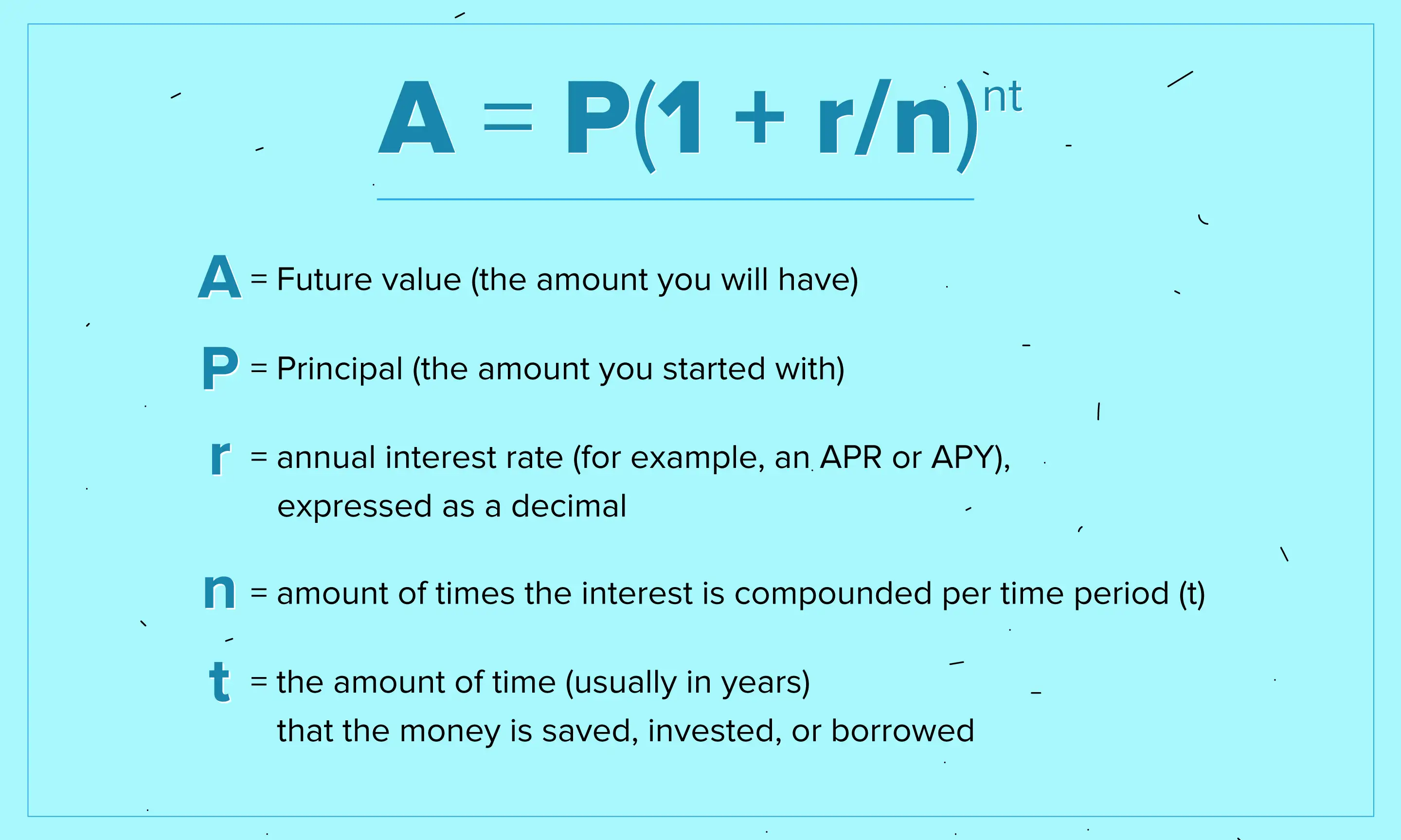

To calculate compound interest on a loan, you need to understand the concept of interest rates, principal amounts, and compounding periods. The formula for calculating compound interest is A = P(1 + r/n)^(nt), where A is the amount of money accumulated after n years, including interest, P is the principal amount, r is the annual interest rate, n is the number of times that interest is compounded per year, and t is the time the money is invested or borrowed for, in years.

Understanding the Formula

The formula for calculating compound interest is based on the concept of exponential growth, where the interest is added to the principal amount at regular intervals, causing the interest to earn interest itself. To calculate compound interest, you need to know the principal amount, the annual interest rate, the compounding frequency, and the time period. The formula can be broken down into the following steps:

- Determine the principal amount and the annual interest rate.

- Choose the compounding frequency, which can be annually, quarterly, monthly, or daily.

- Calculate the total amount using the formula A! = P(1 + r/n)^(nt).

Types of Compounding Frequencies

The compounding frequency refers to how often the interest is added to the principal amount. The most common compounding frequencies are annually, quarterly, monthly, and daily. Each compounding frequency has a different effect on the total amount of interest earned. For example, daily compounding will result in a higher total amount than annually compounding, given the same principal amount and annual interest rate.

- Annually compounding adds interest to the principal amount once a year.

- Quarterly compounding adds interest to the principal amount four times a year.

- Monthly compounding adds interest to the principal amount twelve times a year.

Effects of Compounding Periods

The compounding period refers to the length of time between compounding frequencies. A longer compounding period will result in less interest earned, while a shorter compounding period will result in more interest earned. For example, monthly compounding will result in more interest earned than quarterly compounding, given the same principal amount and annual interest rate.

- A shorter compounding period will result in more interest earned.

- A longer compounding period will result in less interest earned.

- The compounding period can significantly impact the total amount of interest earned.

Calculating Compound Interest on a Loan

To calculate compound interest on a loan, you need to know the loan amount, the annual interest rate, the compounding frequency, and the loan term. You can use a calculator or a spreadsheet to calculate the monthly payments and the total interest paid over the life of the loan.

- Determine the loan amount and the annual interest rate.

- Choose the compounding frequency, which can be annually, quarterly, monthly, or daily.

- Calculate the monthly payments using a calculator or a spreadsheet.

Importance of Understanding Compound Interest

Understanding compound interest is crucial for making informed decisions about loans and investments. It can help you save money by choosing the right compounding frequency and interest rate. Additionally, it can help you earn more interest on your savings and investments.

- Understanding compound interest can help you make informed decisions about loans and investments.

- It can help you save money by choosing the right compounding frequency and interest rate.

- It can help you earn more interest on your savings and investments.

What is 6% interest on a $30,000 loan?

To calculate the interest on a $30,000 loan with a 6% interest rate, you can use the formula: Interest = Principal x Rate. In this case, the principal is $30,000 and the rate is 6%. So, the interest would be $30,000 x 0.06 = $1,800 per year.

Understanding Interest Rates

The interest rate is a critical factor in determining the total cost of a loan. A 6% interest rate means that for every $100 borrowed, the borrower will pay $6 in interest per year. This can add up quickly, especially for larger loans like the $30,000 example. Here are some key points to consider:

- The interest rate is expressed as a percentage of the principal amount.

- A higher interest rate means more interest paid over the life of the loan.

- Interest rates can be fixed or variable, depending on the loan terms.

Calculating Total Interest Paid

To calculate the total interest paid over the life of the loan, you need to know the loan term, which is the length of time the borrower has to repay the loan. For example, if the $30,000 loan has a 5-year term, the total interest paid would be $1,800 per year x 5 years = $9,000. Here are some steps to follow:

- Determine the loan term in years.

- Calculate the annual interest using the formula: Interest = Principal x Rate.

- Multiply the annual interest by the loan term to get the total interest paid.

Impact of Interest on Loan Repayment

The interest on a loan can significantly impact the borrower's ability to repay the loan. A higher interest rate means larger monthly payments, which can be a burden for borrowers with limited income. Here are some factors to consider:

- The interest rate affects the monthly payment amount.

- A higher interest rate means more of the monthly payment goes towards interest rather than principal.

- Borrowers should consider the total cost of the loan, including interest, when deciding whether to take out a loan.

Types of Interest Rates

There are two main types of interest rates: fixed and variable. A fixed interest rate remains the same over the life of the loan, while a variable interest rate can change based on market conditions. Here are some key differences:

- A fixed interest rate provides predictable monthly payments.

- A variable interest rate may offer a lower initial interest rate, but it can increase over time.

- Borrowers should carefully consider the risks and benefits of each type of interest rate.

Strategies for Managing Interest Payments

Borrowers can use several strategies to manage their interest payments, such as making extra payments or refinancing the loan. Here are some options to consider:

- Making extra payments can help reduce the principal balance and lower interest payments.

- Refinancing the loan to a lower interest rate can save money on interest payments.

- Borrowers should carefully review their loan terms and consider seeking professional advice before making any changes.

What is the compound interest on $2500 at 6.75% compounded daily for 20 days?

To calculate the compound interest on $2500 at 6.75% compounded daily for 20 days, we need to use the formula for compound interest: A = P(1 + r/n)^(nt), where A is the amount of money accumulated after n years, including interest, P is the principal amount, r is the annual interest rate (in decimal), n is the number of times that interest is compounded per year, and t is the time the money is invested for in years. However, since the interest is compounded daily for 20 days, we will use the daily interest rate and the number of days.

Calculating Daily Interest Rate: The daily interest rate can be calculated by dividing the annual interest rate by 365 (days in a year). So, the daily interest rate is 6.75%/365 = 0.01848 (in decimal).

Understanding Compound Interest Formula

The compound interest formula is A = P(1 + r/n)^(nt), but in this case, we will use A = P(1 + r)^n, where r is the daily interest rate and n is the number of days. This is because the interest is compounded daily. The principal amount P is $2500, the daily interest rate r is 0.01848 (6.75%/365), and the number of days n is 20. The formula becomes A = 2500(1 + 0.01848)^20.

- The principal amount is $2500.

- The daily interest rate is 0.01848 (6.75%/365).

- The number of days is 20.

Calculating Compound Interest

To calculate the compound interest, we first need to calculate the amount of money accumulated after 20 days, including interest. Using the formula A = 2500(1 + 0.01848)^20, we get A = 2500(1.01848)^20 ≈ 2500 1.04145 ≈ 2603.61. The compound interest is then calculated by subtracting the principal amount from the accumulated amount: Compound Interest = A - P = 2603.61 - 2500 = $103.61.

- The accumulated amount is $2603.61.

- The compound interest is $103.61.

- The interest rate is 6.75%.

Importance of Compounding Frequency

The compounding frequency plays a crucial role in calculating the compound interest. In this case, the interest is compounded daily, which means that the interest is added to the principal amount every day. This results in a higher accumulated amount compared to if the interest were compounded monthly or annually. The daily compounding frequency allows the interest to grow exponentially, resulting in a higher compound interest.

- Daily compounding frequency results in higher accumulated amount.

- Monthly or annual compounding frequency results in lower accumulated amount.

- Exponential growth occurs due to daily compounding.

Effects of Interest Rate on Compound Interest

The interest rate has a significant impact on the compound interest. A higher interest rate results in a higher compound interest, while a lower interest rate results in a lower compound interest. In this case, the interest rate is 6.75%, which is relatively high. This results in a higher compound interest of $103.61.

- A higher interest rate results in higher compound interest.

- A lower interest rate results in lower compound interest.

- The interest rate of 6.75% results in a compound interest of $103.61.

Real-World Applications of Compound Interest

Compound interest has numerous real-world applications in finance and banking. It is used to calculate the interest on savings accounts, investments, and loans. Understanding compound interest is essential for making informed decisions about investments and loans. In this case, the compound interest on $2500 at 6.75% compounded daily for 20 days is $103.61, which can be used to compare investment options or evaluate loan offers.

- Compound interest is used in savings accounts.

- Compound interest is used in investments and loans.

- Understanding compound interest is essential for informed decision-making.

Frequently Asked Questions (FAQs)

What is the Loan Compound Interest Calculator and how does it work?

The Loan Compound Interest Calculator is a financial tool designed to help individuals calculate the interest accrued on a loan over a specified period of time. It takes into account the principal amount, interest rate, and compounding frequency to provide an accurate calculation of the total interest paid over the life of the loan. The calculator uses the formula for compound interest, which is A = P(1 + r/n)^(nt), where A is the amount of money accumulated after n years, including interest, P is the principal amount, r is the annual interest rate, n is the number of times that interest is compounded per year, and t is the time the money is invested or borrowed for, in years. By using this calculator, individuals can get a clear understanding of how compound interest works and how it can impact their loan payments.

How do I use the Loan Compound Interest Calculator to calculate my loan payments?

To use the Loan Compound Interest Calculator, you need to enter the principal amount, interest rate, loan term, and compounding frequency. The principal amount is the initial amount borrowed, the interest rate is the rate at which interest is charged, the loan term is the length of time the money is borrowed for, and the compounding frequency is how often interest is calculated and added to the principal amount. Once you have entered this information, the calculator will provide you with a detailed breakdown of the total interest paid over the life of the loan, the monthly payment amount, and the total amount paid. You can also use the calculator to compare different loan scenarios and see how different interest rates and compounding frequencies can impact your loan payments. By using the Loan Compound Interest Calculator, you can make informed decisions about your loan and ensure that you are getting the best possible deal.

What are the benefits of using the Loan Compound Interest Calculator?

There are several benefits to using the Loan Compound Interest Calculator. One of the main benefits is that it allows you to compare different loan options and see which one is the best fit for your needs. By using the calculator, you can see how different interest rates and compounding frequencies can impact your loan payments, and make an informed decision about which loan to choose. Another benefit is that the calculator helps you to understand the true cost of borrowing, by providing a detailed breakdown of the total interest paid over the life of the loan. This can help you to avoid hidden fees and unexpected costs, and ensure that you are getting a fair deal. Additionally, the calculator can help you to plan your finances and make informed decisions about your loan, by providing you with a clear understanding of your monthly payment amount and the total amount paid.

How can I use the Loan Compound Interest Calculator to plan my finances and make informed decisions about my loan?

The Loan Compound Interest Calculator can be a valuable tool in planning your finances and making informed decisions about your loan. By using the calculator, you can get a clear understanding of your monthly payment amount and the total amount paid over the life of the loan. This can help you to budget and plan your finances, and ensure that you have enough money set aside each month to make your loan payments. Additionally, the calculator can help you to compare different loan options and see which one is the best fit for your needs. By using the calculator, you can see how different interest rates and compounding frequencies can impact your loan payments, and make an informed decision about which loan to choose. You can also use the calculator to experiment with different scenarios, such as paying off your loan early or increasing your monthly payment amount, and see how these changes can impact your loan. By using the Loan Compound Interest Calculator in this way, you can take control of your finances and make informed decisions about your loan.

Deja una respuesta

Entradas Relacionadas