Is there a way to make SaaS a capital expense?

Software as a Service (SaaS) has become a cornerstone of modern business operations, offering flexibility, scalability, and cost efficiency. However, its classification as an operational expense (OpEx) can pose challenges for companies seeking to optimize their financial strategies. Many organizations prefer capital expenses (CapEx) for long-term investments, as they align with asset acquisition and depreciation benefits. This raises the question: Is there a way to make SaaS a capital expense? Exploring this possibility involves understanding accounting principles, tax regulations, and innovative financial structuring. This article delves into potential strategies businesses can consider to reclassify SaaS expenditures, balancing operational needs with financial optimization.

- Is There a Way to Make SaaS a Capital Expense?

- Can SaaS be a capital expense?

- Can you capitalize SaaS costs?

- Can software be a capital expense?

- Is software subscription CapEx or OpEx?

-

Frequently Asked Questions (FAQ)

- Can SaaS subscriptions be classified as a capital expense?

- What are the key factors to consider when classifying SaaS as a capital expense?

- How does the treatment of SaaS differ between capital expenses and operating expenses?

- Are there specific accounting standards that allow SaaS to be treated as a capital expense?

Is There a Way to Make SaaS a Capital Expense?

Yes, there are ways to classify Software as a Service (SaaS) as a capital expense (CapEx) rather than an operating expense (OpEx), although it depends on specific accounting practices and the nature of the SaaS agreement. Typically, SaaS is treated as an OpEx because it is a subscription-based service. However, under certain conditions, it can be capitalized, especially if the software meets specific criteria for long-term value and asset classification.

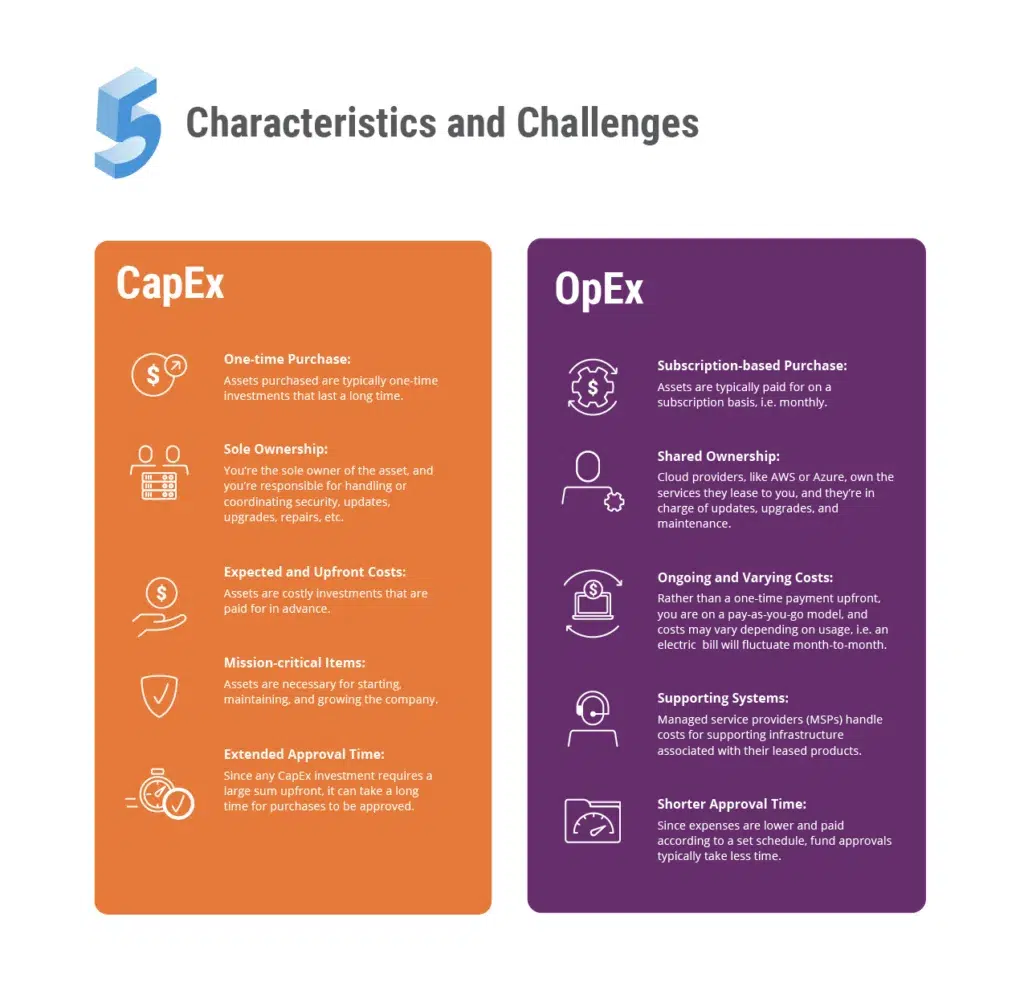

Understanding Capital Expenses vs. Operating Expenses

Capital expenses (CapEx) refer to costs incurred to acquire or upgrade long-term assets, while operating expenses (OpEx) are ongoing costs for running a business. SaaS is usually categorized as an OpEx because it is a recurring subscription. However, if the SaaS provides long-term value or is integral to creating a long-term asset, it may qualify as a CapEx. For example, if the SaaS is used to develop a proprietary platform, the costs could be capitalized.

| CapEx | OpEx |

|---|---|

| Long-term asset acquisition | Recurring operational costs |

| Depreciated over time | Expensed immediately |

Criteria for Capitalizing SaaS Costs

To capitalize SaaS costs, the software must meet specific criteria, such as providing long-term value or being part of a larger project. For instance, if the SaaS is used to develop a custom application or platform, the costs may be capitalized. Additionally, the software must have a useful life beyond one year, and the company must demonstrate that it will derive future economic benefits from it.

| Criteria | Description |

|---|---|

| Long-term value | The software must provide benefits beyond one year. |

| Future economic benefits | The company must prove it will gain value from the software. |

Accounting Standards and SaaS Capitalization

Accounting standards like GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards) provide guidelines for capitalizing software costs. Under these standards, SaaS can be capitalized if it meets the criteria for an intangible asset. For example, if the SaaS is used to create a proprietary tool, the costs may be capitalized and amortized over its useful life.

| Standard | Guidelines |

|---|---|

| GAAP | Allows capitalization if the software meets asset criteria. |

| IFRS | Similar to GAAP, with specific rules for intangible assets. |

Examples of SaaS as a Capital Expense

One example of SaaS being treated as a CapEx is when a company uses it to develop a custom software platform. The costs associated with the SaaS subscription during the development phase can be capitalized and amortized over the platform's useful life. Another example is when SaaS is used to create a proprietary database or tool that provides long-term value to the business.

| Example | Explanation |

|---|---|

| Custom software development | SaaS costs are capitalized during the development phase. |

| Proprietary database creation | SaaS costs are amortized over the database's useful life. |

Challenges in Capitalizing SaaS Costs

One of the main challenges in capitalizing SaaS costs is proving that the software meets the criteria for a long-term asset. Additionally, the process requires detailed documentation and adherence to strict accounting standards. Companies must also consider the impact on financial statements, as capitalizing costs can affect metrics like EBITDA and net income.

| Challenge | Impact |

|---|---|

| Proving long-term value | Requires detailed documentation and justification. |

| Adherence to accounting standards | Must follow GAAP or IFRS guidelines strictly. |

Can SaaS be a capital expense?

Understanding SaaS and Capital Expenses

Software as a Service (SaaS) is typically considered an operating expense (OpEx) rather than a capital expense (CapEx). This is because SaaS is usually purchased on a subscription basis, with payments made regularly over time rather than as a one-time upfront cost. However, there are scenarios where SaaS can be classified as a capital expense, depending on the accounting practices and the nature of the software.

- Subscription Model: SaaS is generally billed monthly or annually, aligning it with operating expenses.

- Upfront Costs: If a SaaS provider requires a significant upfront payment, it might be treated as a capital expense.

- Customization: If the SaaS solution requires extensive customization, the associated costs could be capitalized.

When Can SaaS Be Treated as a Capital Expense?

SaaS can be treated as a capital expense under specific circumstances, particularly when the software meets certain criteria for capitalization. This often involves the software being used to create or enhance a long-term asset.

- Long-Term Use: If the SaaS is expected to provide value for more than one year, it may qualify as a capital expense.

- Significant Investment: Large upfront payments or investments in the software can justify capitalization.

- Asset Creation: If the SaaS is used to develop or improve a long-term asset, it may be capitalized.

Accounting Standards and SaaS

Accounting standards play a crucial role in determining whether SaaS can be classified as a capital expense. Different standards, such as GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards), have specific guidelines for capitalization.

- GAAP Guidelines: Under GAAP, costs that provide future economic benefits can be capitalized.

- IFRS Guidelines: IFRS also allows for capitalization if the software meets the criteria for an intangible asset.

- Amortization: Capitalized SaaS costs are typically amortized over their useful life.

Tax Implications of SaaS as a Capital Expense

Treating SaaS as a capital expense can have significant tax implications. Capital expenses are usually depreciated or amortized over time, which can affect a company's taxable income.

- Depreciation: Capitalized SaaS costs may be depreciated over their useful life, reducing taxable income.

- Tax Deductions: Operating expenses are typically fully deductible in the year they are incurred, whereas capital expenses are spread out over several years.

- Tax Planning: Companies may choose to capitalize SaaS to manage their tax liabilities more effectively.

Practical Considerations for SaaS Capitalization

When deciding whether to treat SaaS as a capital expense, companies must consider practical factors such as the nature of the software, the payment structure, and the potential impact on financial statements.

- Payment Structure: The way SaaS is paid for (e.g., monthly vs. upfront) can influence whether it is treated as an operating or capital expense.

- Financial Reporting: Capitalizing SaaS can affect key financial metrics, such as EBITDA and net income.

- Internal Policies: Companies should establish clear policies for determining when SaaS costs should be capitalized.

Can you capitalize SaaS costs?

What Does It Mean to Capitalize SaaS Costs?

Capitalizing SaaS costs refers to recording these expenses as an asset on the balance sheet rather than expensing them immediately. This is typically done when the SaaS solution provides long-term value or meets specific criteria under accounting standards like GAAP or IFRS.

- Capitalization involves spreading the cost over the useful life of the SaaS product.

- It requires the SaaS solution to meet certain capitalization criteria, such as providing future economic benefits.

- This approach aligns with the matching principle in accounting, ensuring costs are recognized in the same period as the benefits.

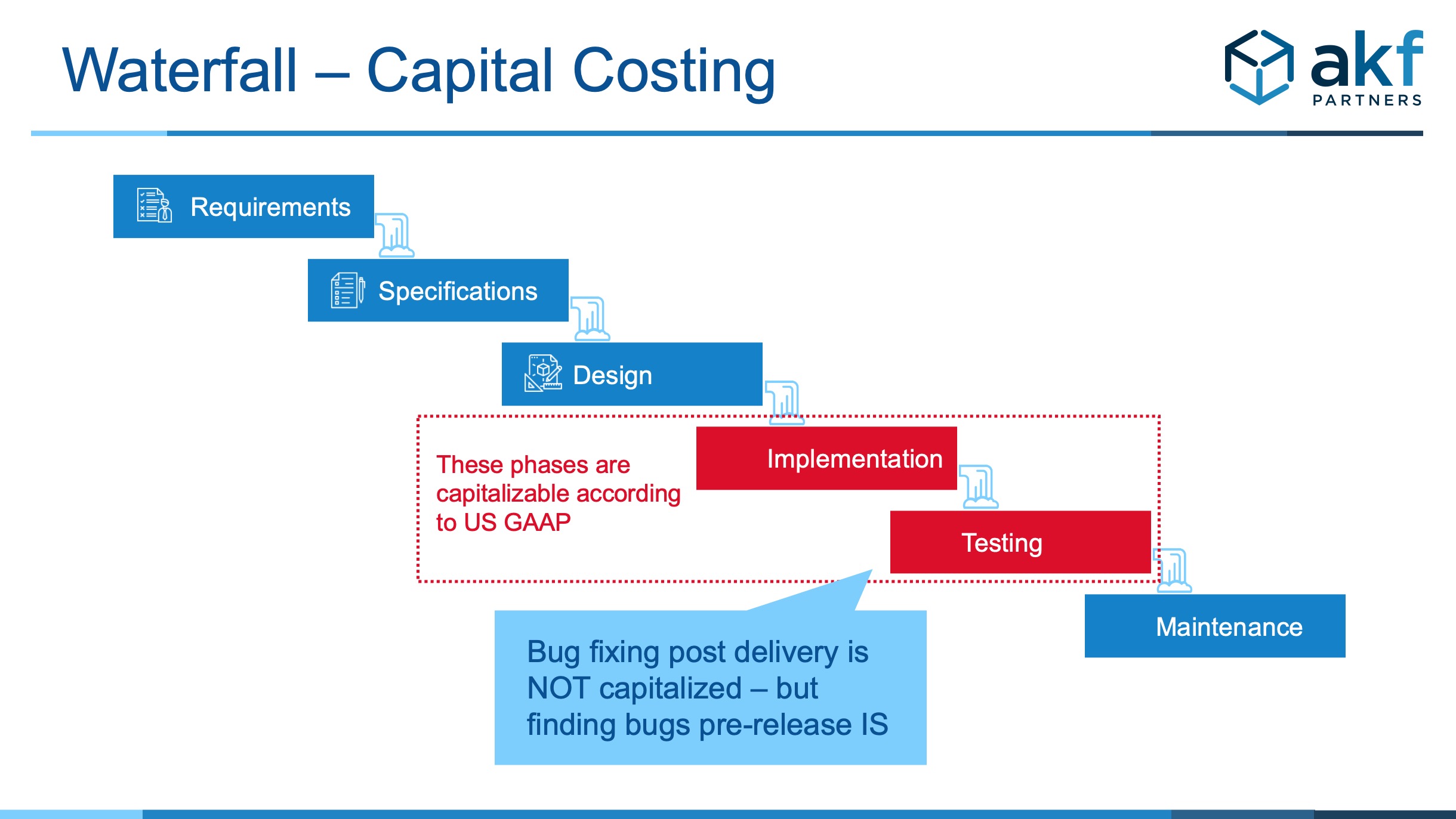

When Can SaaS Costs Be Capitalized?

SaaS costs can be capitalized under specific conditions, such as when the software is used to develop or enhance internal-use software. The following points outline the key scenarios:

- If the SaaS is used during the application development stage of an internal-use software project.

- When the costs are directly attributable to making the software ready for its intended use.

- If the SaaS provides long-term benefits that extend beyond the current accounting period.

What Are the Accounting Standards for Capitalizing SaaS Costs?

Accounting standards like GAAP and IFRS provide guidelines for capitalizing SaaS costs. These standards ensure consistency and transparency in financial reporting.

- Under GAAP, SaaS costs can be capitalized if they meet the criteria in ASC 350-40 (Internal-Use Software).

- IFRS requires that costs be capitalized if they meet the definition of an intangible asset under IAS 38.

- Both standards emphasize the need for future economic benefits to justify capitalization.

What Are the Benefits of Capitalizing SaaS Costs?

Capitalizing SaaS costs offers several advantages for businesses, particularly in terms of financial reporting and tax implications.

- It improves profitability metrics by spreading costs over multiple periods.

- Capitalization can lead to tax deferrals, as expenses are recognized over time rather than immediately.

- It provides a more accurate representation of the company's financial position by aligning costs with benefits.

What Are the Challenges of Capitalizing SaaS Costs?

While capitalizing SaaS costs has benefits, it also presents certain challenges that businesses must consider.

- Determining the useful life of the SaaS product can be subjective and complex.

- There is a risk of overcapitalization, which can distort financial statements.

- Compliance with accounting standards requires careful documentation and justification.

Can software be a capital expense?

What is a Capital Expense?

A capital expense (CapEx) refers to funds used by a company to acquire, upgrade, or maintain physical or intangible assets that will provide benefits over a long period. These expenses are typically significant and are capitalized on the balance sheet rather than being expensed immediately. Examples include purchasing machinery, buildings, or software that will be used for more than one year.

- Capital expenses are investments in long-term assets.

- They are recorded on the balance sheet and depreciated or amortized over time.

- Unlike operational expenses, they are not fully deducted in the year they are incurred.

Can Software Be Considered a Capital Expense?

Yes, software can be considered a capital expense if it meets certain criteria. Generally, if the software is purchased or developed for long-term use and provides value over multiple years, it can be capitalized. This includes enterprise software, custom-developed applications, or significant upgrades to existing systems.

- Software must have a useful life of more than one year to qualify as a capital expense.

- It should provide long-term economic benefits to the business.

- Costs associated with implementation, customization, and training may also be capitalized.

How to Determine if Software is a Capital Expense

To determine if software qualifies as a capital expense, businesses must evaluate its purpose, expected lifespan, and cost. Accounting standards, such as GAAP or IFRS, provide guidelines for capitalizing software costs. For example, costs incurred during the development phase of internal-use software can often be capitalized, while maintenance costs are typically expensed.

- Assess whether the software has a useful life exceeding one year.

- Determine if the software is integral to business operations or revenue generation.

- Follow accounting standards to ensure proper classification and treatment.

Examples of Software as a Capital Expense

Examples of software that can be treated as a capital expense include enterprise resource planning (ERP) systems, customer relationship management (CRM) software, and custom-built applications. These types of software are typically expensive, require significant implementation efforts, and are used for multiple years.

- ERP systems like SAP or Oracle are often capitalized due to their long-term utility.

- CRM platforms such as Salesforce may qualify if they are customized for specific business needs.

- Custom-developed software tailored to unique business processes is also a common capital expense.

Tax Implications of Capitalizing Software

Capitalizing software as a capital expense has important tax implications. Instead of deducting the entire cost in the year of purchase, businesses can amortize the expense over the software's useful life, typically 3-5 years. This can help reduce taxable income over time and align expenses with the benefits received from the software.

- Amortization allows businesses to spread the cost of software over its useful life.

- This approach can result in lower taxable income in the initial years.

- Proper documentation and adherence to tax regulations are essential to avoid penalties.

Is software subscription CapEx or OpEx?

Understanding CapEx and OpEx in Software Subscriptions

Software subscriptions are generally classified as Operating Expenses (OpEx) rather than Capital Expenditures (CapEx). This is because software subscriptions are typically recurring payments for services or access to software, rather than a one-time purchase of a tangible asset. Here’s why:

- Recurring Payments: Software subscriptions involve ongoing payments, which align with the nature of OpEx.

- No Ownership: Subscriptions do not grant ownership of the software, making them operational costs rather than capital investments.

- Flexibility: OpEx allows businesses to adjust their expenses based on usage, which is common with subscription models.

Key Differences Between CapEx and OpEx in Software

Understanding the distinction between CapEx and OpEx is crucial for financial planning. Here’s how they differ in the context of software:

- Capital Expenditures (CapEx): These are one-time investments in assets that provide long-term value, such as purchasing software licenses outright.

- Operating Expenses (OpEx): These are ongoing costs required to maintain daily operations, such as software subscription fees.

- Financial Impact: CapEx affects the balance sheet, while OpEx impacts the income statement.

Why Software Subscriptions Are Typically OpEx

Software subscriptions are classified as OpEx due to their nature and financial treatment. Here’s a detailed explanation:

- No Asset Creation: Subscriptions do not result in the creation of a tangible or intangible asset on the balance sheet.

- Short-Term Commitment: Subscriptions are often short-term, aligning with the operational expense model.

- Predictable Costs: OpEx allows businesses to predict and manage costs more effectively, which is ideal for subscription-based services.

Exceptions Where Software Subscriptions Might Be CapEx

While rare, there are scenarios where software subscriptions could be considered CapEx. Here’s when this might apply:

- Long-Term Contracts: If a subscription agreement spans several years and includes significant upfront costs, it might be treated as CapEx.

- Custom Development: Subscriptions that include custom software development or significant modifications may qualify as CapEx.

- Ownership Transfer: If the subscription includes clauses for eventual ownership of the software, it could be classified as CapEx.

Financial Reporting Implications of Software Subscriptions

The classification of software subscriptions as OpEx or CapEx has significant implications for financial reporting. Here’s how:

- OpEx Reporting: Subscriptions classified as OpEx are expensed immediately, reducing net income in the period they are incurred.

- CapEx Reporting: If classified as CapEx, the cost is capitalized and depreciated over time, impacting the balance sheet and income statement differently.

- Tax Implications: OpEx can often be fully deducted in the year they are incurred, while CapEx is depreciated over several years, affecting tax liabilities.

Frequently Asked Questions (FAQ)

Can SaaS subscriptions be classified as a capital expense?

Yes, under certain circumstances, SaaS subscriptions can be classified as a capital expense (CapEx). This typically occurs when the SaaS solution is considered a long-term investment that provides value over multiple years. For example, if the SaaS platform is integral to the company's operations and is used to develop or enhance a product or service, it may qualify as a capital expense. However, this classification depends on the specific accounting standards and regulations followed by the organization, such as GAAP or IFRS.

What are the key factors to consider when classifying SaaS as a capital expense?

When determining whether a SaaS subscription can be classified as a capital expense, several factors must be considered. These include the duration of the contract, the purpose of the SaaS (e.g., whether it is used for long-term projects or operational efficiency), and the accounting standards applicable to the business. Additionally, the ability to capitalize costs often depends on whether the SaaS platform is used to create or enhance an asset that will generate future economic benefits.

How does the treatment of SaaS differ between capital expenses and operating expenses?

The treatment of SaaS subscriptions as either a capital expense (CapEx) or an operating expense (OpEx) has significant implications for financial reporting. When classified as a capital expense, the cost is amortized over its useful life, reflecting its long-term value. In contrast, operating expenses are fully deducted in the year they are incurred. This distinction affects a company's profitability metrics, tax liabilities, and cash flow statements, making it crucial to determine the appropriate classification based on the SaaS's role in the business.

Are there specific accounting standards that allow SaaS to be treated as a capital expense?

Yes, certain accounting standards provide guidelines for treating SaaS subscriptions as a capital expense. For instance, under IFRS 16 and ASC 842, SaaS contracts that meet specific criteria, such as being used to create or enhance an asset, may qualify for capitalization. However, the rules can be complex, and businesses often need to consult with accounting professionals to ensure compliance and proper classification. It's also important to note that these standards may evolve, so staying updated on regulatory changes is essential.

Deja una respuesta

Entradas Relacionadas